A Texas Stowers Demand corners a commercial insurance carrier and legally strips away its ability to lowball your catastrophic injury claim after a severe collision.

The corporate adjuster handling your Bexar County crash is already deploying delay tactics. They scrutinize your statements to manufacture shared fault, pushing rapid payouts that arrive before you finish medical treatment to cap their financial exposure.

They rely on a staggering volume of victims folding under pressure. According to the National Safety Council, 114,552 large trucks were involved in injury crashes in 2023 alone. Behind that statistic is a deceptive corporate playbook designed to protect negligent trucking profits at your family’s expense.

You must shift the financial risk directly onto the insurance corporation. A valid demand offers a full, unconditional release of the negligent driver but requires strict statutory compliance and a minimum fifteen-day response window. Miss one technical requirement, and the carrier easily escapes liability.

As a client of Trevino Injury Law, you’ll get the best semi truck accident lawyer to draft undeniable demands and corner the carrier. Call 210-TREVINO for a free case review. You pay nothing unless we win. Se Habla Español.

What Constitutes a Valid Stowers Demand in Texas?

A Stowers Demand in Texas must explicitly offer to release the negligent trucking company from all liability in exchange for a settlement amount equal to or less than its commercial insurance policy limits. This strict compliance is required by the landmark Texas precedent American Physicians Insurance Exchange v. Garcia, 876 S.W.2d 842 (Tex. 1994), which established that a valid demand must fall entirely within policy limits and include an unconditional release of the at-fault driver.

To trigger the Stowers doctrine under Texas law, the demand must meet strict legal criteria established by the Texas Supreme Court. The demand must be made in writing, clearly state the terms of the settlement, and provide the insurance company a reasonable time to respond.

If a commercial truck driver causes a catastrophic collision near the South Texas Medical Center, our firm meticulously drafts this demand to include the full picture of recoverable damages after a catastrophic commercial collision and how a Life Care Plan proves the true cost of your injuries, demonstrating that a Bexar County jury would likely award damages far exceeding the policy limits.

Insurance adjusters will scrutinize every word, looking for a loophole to escape liability. This technical precision is why you need a plaintiff trial lawyer who understands the exact statutory language required to corner the carrier.

What Are the Red Flags of a Bad Insurance Settlement Offer?

The most glaring red flags of a bad insurance settlement offer include rapid payouts that arrive before you finish your medical treatment, complete failure to account for your future lost wages, and lowball settlement amounts that completely ignore your permanent physical impairment and daily suffering.

Commercial insurers rely on your financial desperation. If an adjuster offers a quick check right after a San Antonio commercial crash, they are attempting to buy off your claim before the true extent of your injuries is known. Other prominent red flags include:

- Rapid payouts arrive before medical treatment concludes.

- Failing to account for future lost wages or diminished earning capacity.

- Ignoring permanent physical impairment and pain.

- Shifting comparative fault onto you unjustifiably.

- Refusing to put their valuation methods in writing.

Each red flag corresponds directly to a category of future earning capacity losses in a Texas truck accident claim that a settlement mill will quietly forfeit if you let them.

We aggressively reject these lowball tactics and use them as further evidence of the carrier’s bad-faith handling of your claim. After identifying these deceptive tactics, you must understand the legal timeline for forcing the insurer to act.

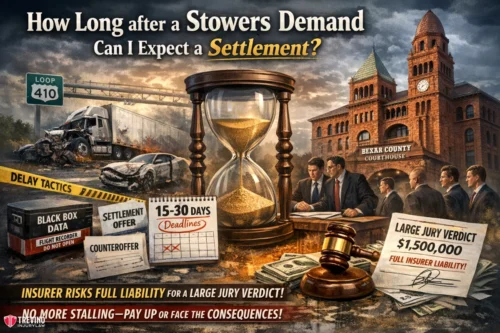

How Long after a Stowers Demand Can I Expect a Settlement?

After a formal Stowers Demand is delivered, Texas law grants the commercial insurance company a strict window of at least fifteen days to either accept the settlement, reject it, or issue a counteroffer based on the comprehensive medical and crash evidence provided by your legal team.

During this critical window, the insurance carrier’s legal defense team must evaluate the evidence we have gathered, including preserved black box data and expert medical testimony. If they realize our Plaintiff Trial Lawyers are fully prepared to take the case to the Bexar County Courthouse, they will often capitulate and pay up to the policy limits within that 15- to 30-day timeframe.

However, carriers like Progressive or State Farm may attempt to stall your claim following a severe accident on Loop 410. We do not tolerate delay tactics. If they fail to accept a reasonable demand within the deadline, the Stowers protection is triggered. This means the insurer can now be held financially responsible for the full amount of a future jury verdict, even if it exceeds their original policy limits.

What Are the Signs of a Good Settlement Offer?

A good settlement offer fully covers your past medical bills, guarantees reliable funding for your comprehensive Life Care Plan, compensates you for all lost earning capacity, and includes substantial non-economic damages to properly address your permanent physical impairment, daily agony, and long-term pain and suffering.

A legitimate offer from a trucking company respects the full severity of your catastrophic injuries. It will align with the comprehensive financial roadmap our medical experts construct. When we secured a $17 Million settlement in an 18-wheeler wrongful death case, it was because the offer appropriately reflected the profound, lifelong loss suffered by the family.

A good offer leaves no future medical expense to chance and provides true financial stability. Getting to this successful point requires avoiding the early traps set by the defense team right after the crash.

What Is the Biggest Mistake People Make When Dealing with a Trucking Insurance Adjuster?

The biggest mistake injury victims make when dealing with a trucking insurance adjuster is providing a recorded statement without legal representation, allowing the corporate carrier to use deceptive questioning to twist your words, manufacture shared fault, and intentionally minimize their financial liability for the crash.

Insurance adjusters are highly trained corporate negotiators whose sole job is to protect the trucking company’s profits by paying you as little as possible. When you are hit by a commercial truck on Bandera Road, rapid response teams are deployed immediately. If you speak to them, they will use deceptive questioning to make you admit partial fault or downplay your injuries.

If you are wondering what not to tell your insurance company, you must never discuss your medical history, speculate on how the crash occurred, or admit any level of guilt, as these statements will ruin your case. By attempting to navigate this process alone, you forfeit your leverage.

A Stowers Demand requires a foundation of undeniable evidence and liability. If you damage your own credibility early on, the insurance company will never take a subsequent settlement demand seriously. To maximize what compensation 18-wheeler accident victims can recover in Texas, you must protect your claim from these specific adjuster traps. Recognizing these common mistakes reveals exactly why trial readiness repairs your leverage against massive insurance corporations.

How Does Taking a Case to Trial Increase Your Stowers Demand Leverage?

Taking a case to trial increases your Stowers Demand leverage because commercial insurance companies fear only plaintiff trial lawyers with a proven history of securing massive jury verdicts that far exceed initial lowball offers, forcing carriers to evaluate the true financial risk of a courtroom defeat.

A demand letter from a high-volume settlement mill carries zero weight because the insurance company knows the lawyer will eventually fold and avoid the courtroom. At Trevino Injury Law, our trial-first mindset is our greatest weapon.

They see concrete results, such as the case of Jose Simon Arriaga Jr., where the defense initially offered a mere $5,000. Instead of accepting it, we took them to court and secured a $536,007 jury verdict, more than 100 times their initial lowball offer. When we issue a formal Stowers Demand, the defense knows we are fully prepared to litigate in South Texas courts.

This verifiable threat of extreme financial exposure is what forces them to pay the policy limits rather than risk a devastating verdict. Understanding this procedural leverage leads directly to the critical question of what supplementary evidence is required to build such an undeniable case.

What Is a Typical Amount for Pain and Suffering in a Commercial Crash?

There is no single typical amount for pain and suffering in a commercial crash, as Texas juries award non-economic damages based entirely on the unique severity, permanence, and daily impact of your specific catastrophic injuries caused by the negligent truck driver.

While economic damages cover objective medical bills, pain and suffering compensate you for the loss of your quality of life. For example, in our $7.9 Million jury verdict for a client who suffered a crushed foot and amputated toe, a significant portion of the award reflected the permanent physical impairment and daily agony caused by the negligent commercial operation.

We use top medical specialists to vividly document this invisible suffering, ensuring the Stowers Demand accurately captures the full human cost of the collision.

Can You Send a Stowers Demand Without a Trial Lawyer?

No, you cannot execute a Stowers Demand without a trial lawyer because it requires strict statutory formatting and a credible threat of litigation.

Does a Stowers Demand Guarantee the Insurance Company Will Pay?

No, a Stowers Demand does not guarantee payment, but it places the insurance carrier in severe legal jeopardy if they reject your valid settlement offer.

Understanding these critical legal requirements clarifies how this specific document differs from ordinary negotiation tactics.

What Happens When an Insurance Company Refuses a Reasonable Settlement?

Under Texas insurance law, insurance companies have a duty to act in good faith when evaluating a claim within policy limits. If an insurer unreasonably rejects a Stowers demand and refuses a reasonable settlement offer, it is actively choosing to protect its profit margins over its insured’s financial safety.

When a company refuses to settle a claim within the insured’s policy limits, it forces the injured parties to go to trial. If the case goes to trial because of the insurer failing to settle, and the jury awards damages in excess of the policy limits, the insurer can be held responsible for the entire verdict.

Because the Texas Supreme Court held that an insurer to act in bad faith assumes this massive financial risk, our trial lawyers are always fully prepared to take the case to trial to ensure your family receives a fair settlement or the entire verdict you deserve.

How Do Stowers Demands Compare to Standard Settlement Letters?

While a standard settlement letter merely initiates informal negotiations regarding your injuries, a valid Stowers Demand is a highly specific Texas legal trap that triggers strict liability consequences, potentially forcing the commercial insurance company to pay amounts far exceeding its policy limits.

Standard letters often lack concrete deadlines and fail to legally expose the insurer’s corporate assets. In contrast, a Stowers Demand utilizes the strict precedent set by the Texas Supreme Court to proactively protect your family. It explicitly offers a full and unconditional release of the negligent truck driver in exchange for the policy limits within a non-negotiable timeframe.

| Feature | Standard Settlement Letter | Texas Stowers Demand |

| Primary Purpose | Initiates general financial negotiations | Triggers strict legal liability limits |

| Response Deadline | Open-ended or informal timeline | Strict statutory minimum of 15 days |

| Legal Consequence | None if the insurer rejects the offer | Insurer liable for excess jury verdicts |

| Required Elements | General summary of damages | Unconditional release for policy limits |

If executed perfectly by a San Antonio personal injury lawyer, it shifts the financial risk of a massive trial verdict directly onto the insurance corporation, rather than the individual truck driver. Recognizing this adversarial shift of financial risk reveals what happens when the defense team completely ignores the trap.

What Happens If an Insurance Company Ignores a Stowers Demand?

If a commercial insurance company negligently ignores a valid Stowers Demand, they breach their legal duty to protect their insured client and become legally responsible for paying the entire jury verdict out of their own pocket. This powerful shift in financial liability originates from the foundational Texas Supreme Court case G.A. Stowers Furniture Co. v. American Indemnity Co., 15 S.W.2d 544 (Tex. Comm’n App. 1929), which firmly established an insurer’s duty to exercise ordinary care in settling claims to protect its insured from financially devastating excess judgments.

This is the ultimate legal power of the Stowers doctrine. If a negligent trucking company carries a $1 million policy, and our firm issues a proper demand for that exact $1 million, which the adjuster ignores, we immediately proceed to trial. If a Bexar County jury then awards you $5 million for your traumatic brain injury, the insurance company cannot simply hide behind its $1 million contractual cap.

They must pay the full $5 million directly to your family because their bad-faith refusal to settle appropriately exposed their client to complete financial ruin. However, while this powerful tool can financially ruin an insurer acting in bad faith, it has very specific legal boundaries that must be respected.

When Does a Stowers Demand Not Apply to a Truck Accident Claim?

A Stowers Demand does not legally apply if liability for the catastrophic commercial truck accident is legitimately disputed in court, or if the specific settlement demand amount exceeds the total available limits outlined in the negligent trucking company’s commercial insurance policy.

The Stowers doctrine protects plaintiffs only when the negligent party’s liability is reasonably clear, and the demand squarely falls within the strict confines of the insurance contract.

Furthermore, it cannot be successfully used if the demand fails to offer a complete, unconditional release of the at-fault driver. Understanding these rigid legal boundaries is exactly why you must hire an experienced Plaintiff Trial Lawyer who thoroughly understands Texas tort law. An improperly drafted demand carries no legal weight, leaving your family’s financial future completely unprotected against corporate greed.

Why Hire a San Antonio 18-Wheeler Accident Lawyer?

With the National Safety Council reporting that 114,552 large trucks were involved in crashes resulting in injuries in 2023 alone, the catastrophic aftermath of a commercial collision on corridors like I-35 requires immediate legal intervention to secure fair financial compensation. Corporate insurance adjusters rely on this staggering volume of annual accidents, using high-pressure tactics to exploit your vulnerability and protect the negligent trucking company’s profits.

Want to Protect the Full Value of Your Claim?

You’ve seen how this affects your case — but this is only one piece of the puzzle. Our 18 Wheeler Accident Lawyer page breaks down what a trial-ready firm does differently.

High-volume settlement mills fold under this pressure and avoid the courtroom entirely. At Trevino Injury Law, we fight for families and hold responsible parties accountable

We leverage a track record of 80+ jury trials and have secured a $17 million settlement to protect our clients at the Bexar County Courthouse. By preserving vital black box data, your San Antonio personal injury lawyers build an undeniable case for trial.

Call 210-TREVINO for a free case review. We operate on a contingency-fee basis. No win, no fee. Se Habla Español.