You survived a devastating collision, but your own insurance company is not actually investigating your severe crash claim. They are intentionally starving you out.

The assigned adjuster runs your medical records through Colossus software to assign arbitrary severity points to your physical impairment, automatically generating an artificial denial. You face a calculated corporate delay tactic. According to the Texas Department of Transportation, San Antonio recorded 39,805 total crashes in 2024. That massive volume creates significant financial exposure, so carriers resort to deceptive trade practices to protect their profits rather than pay what they owe.

Evidence of their bad faith vanishes rapidly. Internal email chains disappear. Adjuster notes get deleted. A Spoliation Letter, a legal demand that prevents the insurance company from destroying evidence, must be issued immediately to lock down their internal claim files. Texas gives you two years from the date of the formal denial to file a lawsuit. After that strict deadline passes, the carrier keeps your money permanently.

At Trevino Injury Law, our personal injury law firm will subpoena any hidden communication logs and force the carrier to pay. Call 210-TREVINO now for a free case review. You pay nothing unless we win. Se Habla Español.

What Constitutes Bad Faith Under the Texas Insurance Code?

Bad faith occurs when an insurance company denies or delays a valid claim when its liability has become reasonably clear, violating Chapter 541 of the Texas Insurance Code. Insurance companies have a duty of “good faith and fair dealing,” which means they cannot prioritize their profits over your valid claim.

Specific violations include failing to attempt to settle your claim fairly once liability is clear, refusing to provide a reasonable explanation for a denial, and misrepresenting policy provisions to confuse policyholders. This is illegal conduct, not just poor customer service, and it gives you the right to sue for damages beyond the original claim value.

As the Texas Supreme Court explained in Arnold v. National County Mutual Fire Insurance Co., “there is a duty on the part of insurers to deal fairly and in good faith with their insureds.” 725 S.W.2d 165, 167 (Tex. 1987). In other words, an insurance company cannot deny, delay, or undervalue a valid claim just to protect its own bottom line. When an insurer has no reasonable basis for its conduct, Texas law gives the policyholder the right to pursue damages beyond the unpaid claim itself.

These violations often stem from automated systems designed to undervalue your loss before a human even reviews it.

Unfair Insurance Practices: Fighting Algorithms and “Colossus”

Major insurers use the “Insurance Defense Playbook” and software algorithms like Colossus or Xactimate to artificially calculate settlement offers based on “severity points” rather than your actual medical reality. These programs are often tuned to ignore human pain and suffering or to flag legitimate medical treatments as “excessive” to justify underpayment of a valid claim.

We know how to “feed” these systems the right medical evidence to trigger higher evaluations, and when that fails, we expose the algorithm’s bias in court by deposing the adjusters who rely on it. When the computer says “no,” and they delay payment, penalties begin to accrue immediately under insurance law.

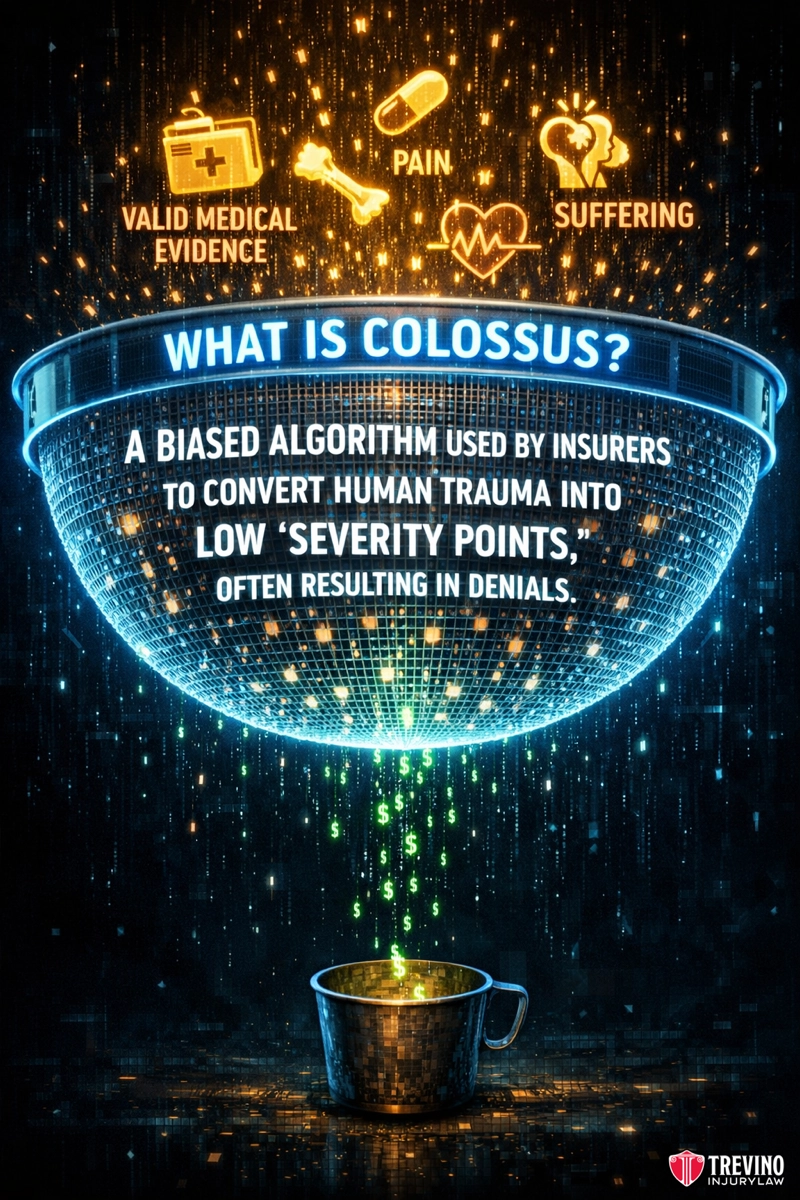

What Is Colossus Insurance Software?

Colossus is a computer program licensed by major insurers (including Allstate, USAA, and others) to estimate the value of bodily injury claims. Theoretically, it standardizes settlement offers; in reality, it is a tool designed to minimize payouts by removing the human element.

The software converts your pain, physical impairment, and medical treatment into arbitrary “severity points” to generate a settlement range. If your medical records do not use the specific keywords or “value drivers” the algorithm recognizes, Colossus effectively “zeros out” legitimate suffering.

We understand the input codes this software requires, and we build your medical evidence to force the algorithm to acknowledge the true severity of your injury.

How the Prompt Payment Act Penalizes Bad Faith Claims Handling

The Texas Prompt Payment of Claims Act (TPPCA) mandates that insurers who delay payment without justification must pay the claim amount plus 18% interest per year and attorney’s fees. While the law is strict, delays remain common, with historical data showing 15,504 complaints filed specifically for claim handling delays (NAIC, 2011).

The timeline is strict: they have 15 days to acknowledge receipt of your claim, 15 days to accept or reject it after receiving the information, and only 5 days to issue payment once accepted. If the insurance company fails to meet these deadlines without a valid statutory reason, the 18% penalty kicks in automatically, turning their delay tactic into a high-interest loan they must repay to you.

Beyond simple interest, knowing violations of these consumer protection laws allow for “treble” damages that punish the insurer.

Can You Sue for Deceptive Trade Practices (DTPA) Violations?

Yes, if we prove the insurer acted “knowingly” or “intentionally,” the Texas Deceptive Trade Practices Act (DTPA) allows you to recover up to three times your actual damages (treble damages). “Knowingly” means they were aware their conduct was false or unfair, while “intentionally” means they meant to cause you harm.

As a victim of insurance bad faith, this turns a standard insurance dispute into a high-stakes lawsuit where the insurance company risks paying triple the original amount, providing massive leverage to force a fair resolution.

Once we identify these violations, we use a specific legal weapon to enforce payment even beyond the policy limits.

How Does the Stowers Doctrine Force Insurers to Pay More Than Policy Limits?

The Stowers Doctrine is a Texas legal precedent that forces an insurance company to pay the full jury verdict, even if it exceeds your policy limits, if they negligently rejected a reasonable settlement offer within those limits. This doctrine shifts the financial risk of a trial from you (or the defendant driver) back onto the insurance company.

If the carrier is acting in bad faith by gambling with your financial safety, rejecting a fair demand, and losing at trial, they are responsible for the entire excess judgment, effectively removing the “cap” on what you can recover.

But how can you sue the other driver’s insurance company when they technically don’t owe you a duty directly?

The “Assignment” Strategy: How We Bypass “Third-Party” Restrictions

While Texas law prevents a third-party victim from directly suing an at-fault driver’s insurer for bad faith, we can overcome this by obtaining an “Assignment of Cause of Action” from the driver after a verdict is rendered. When an insurer refuses to settle and exposes its own client (the at-fault driver) to a massive judgment, it has betrayed that client.

We then offer to release the driver from personal debt if they assign their right to sue the insurer to us, thereby allowing us to step into their shoes and pursue a claim against the insurer directly for the excess verdict.

This adversarial strategy is complex, but the results speak for themselves in our firm’s history of insurance litigation.

Real Results: Turning a $5,000 Offer into a $536,000 Verdict

In a recent case, an insurer offered our client $5,000 on a clear liability claim; we rejected it, filed suit, and secured a $536,000 verdict, over 100 times the initial offer. This case, Jose Simon Arriaga Jr. v. Emily Montemayor, demonstrates that insurance companies often bluff until they face a trial lawyer who refuses to fold.

By proving the insurer’s evaluation was baseless and refusing to accept their lowball “final offer,” we forced a jury to see the truth, resulting in a judgment far exceeding what the adjuster claimed the case was worth. This strategy is particularly effective against certain local non-standard insurers who rely on specific exclusion tactics.

Why You Need a Bad Faith Lawyer to Fight Progressive Group and Non-Standard Carriers

Non-standard carriers like Progressive often rely on specific “Named Driver Exclusions” and aggressive denial tactics, which require a lawyer familiar with their litigation playbook. They frequently deny claims by arguing the person driving the car was not listed on the policy or was specifically excluded, even if they lived in the same household.

Insurers use these tactics more aggressively when they think a settlement mill is on the other side and will fold before meaningful litigation begins.

We investigate further to prove permission, identify ambiguities in the exclusion language, or uncover administrative errors they made that invalidate the exclusion, forcing them to provide coverage they tried to deny.

The stakes are even higher when commercial trucking policies are involved, as the limits and legal complexities increase.

Why Are Commercial and 18-Wheeler Denials Different?

Commercial policies carry much higher limits (often $1M+), leading insurers to fight harder and use “MCS-90” endorsement complexities to deny coverage. Commercial carriers frequently attempt to dodge liability by claiming the driver was acting ‘outside the course and scope of employment.’

The stakes in these commercial disputes are often catastrophic, reflecting the severity of the 686 suspected serious injuries reported in San Antonio in 2024 (TxDOT). We use this to prove the driver was under dispatch or serving the company’s interests, triggering the full commercial policy limits. Whether it is a trucking giant or a stalling adjuster, the solution is ending the delay by forcing them to answer under oath.

How Do We Handle “Ghosting” and Investigative Delays?

When an adjuster stops returning calls, we file a lawsuit to depose them under oath, forcing them to explain their delay before a Bexar County judge. Insurance companies often keep a claim in “pending” status indefinitely, claiming they are “under investigation” or waiting for a police report that is already available.

By filing suit, we end their control over the timeline and use the discovery process to demand their claim file notes, revealing if they were actually investigating or just hoping you would go away.

This aggressive approach halts their stalling, but it raises the ultimate question of when to file your lawsuit.

How Long Do I Have to File a Bad Faith Lawsuit in Texas?

In Texas, the statute of limitations for bad faith claims is generally two years from the date the unfair practice occurred or was reasonably discovered, creating a distinct timeline that may extend beyond your original two-year personal injury filing deadline, depending on when the denial happened.

Unlike your initial car accident claim, which generally expires two years from the crash date, a bad faith claim operates on a different timeline. A bad-faith cause of action ‘accrues,’ meaning the two-year clock starts ticking, on the date the insurance company formally denies the claim.

This distinction is critical for anyone facing bad faith, as it may allow you to file suit even if the statute of limitations on the underlying accident is nearing its end.

However, you should never wait until the last minute, because delays often lead to the “spoliation” of evidence, where critical emails, recorded calls, and adjuster notes are deleted or “lost” by the insurance company before we can subpoena them.

What Is the Process for Filing a Bad Faith Insurance Lawsuit?

The process begins not with a complaint to the state but with a formal demand letter outlining the Texas Insurance Code violations and providing a strict payment deadline, typically 60 days before filing suit. Once this statutory notice period expires, we file a petition in the Bexar County District Courts in downtown San Antonio, officially starting the lawsuit.

This formal legal action is part of a broader litigation landscape, as evidenced by the 95,731 contract case filings in Texas district courts in fiscal year 2024 (Texas Courts, 2024).

The litigation then moves into the discovery phase, where we subpoena the adjuster’s training manuals, email communications, and claim logs to prove their denial was a calculated business decision rather than a legitimate error.

Do I Need a Denial Letter to Sue?

Yes, a written denial letter is critical evidence because it establishes the insurer’s official reason for rejection, which we can then prove is false or pretextual during the litigation process.

Can I Sue My Own Insurance Company for Bad Faith?

Yes, you can sue your own provider (First-Party Bad Faith) if they wrongfully deny your Uninsured/Underinsured Motorist (UM/UIM) or PIP claim, as they owe you the same duty of good faith as any other policyholder.

Does a Bad Faith Claim Cover Attorney Fees?

Yes, the Texas Insurance Code specifically allows policyholders to recover reasonable attorney’s fees if they prevail in a bad-faith lawsuit, ensuring that the cost of fighting for justice does not eat into their compensation.

Bad Faith vs. Negligence: What Is the Difference?

Negligence is a mistake or error in judgment, whereas bad faith means the insurer knew or should have known their denial was unreasonable and did it anyway to save money. A negligent adjuster might misplace a file or miscalculate a total by accident, which is frustrating but not necessarily illegal.

Bad-faith acts are intentional or “knowing” violations, such as a localized carrier like Fred Loya systematically training adjusters to interpret standard insurance policies in ways that deny valid claims for families in Leon Valley or Converse.

What Happens If You Accept the Insurance Company’s First Offer?

If you sign a release for the first offer, you legally waive your right to pursue any further compensation, even if your medical bills turn out to be significantly higher than expected. Insurance adjusters often pressure victims to sign quickly, offering a check that might cover immediate repairs but leaves you responsible for long-term medical costs at major facilities like Stone Oak Methodist or University Hospital.

Once that release is signed, the case is closed forever, and you cannot reopen it to sue for bad faith, no matter how deceptive their original tactics were.

When Is It Too Late to Seek Penalties for a Denied Claim?

It is effectively too late to seek penalties once the two-year statute of limitations expires, or if you have allowed the “spoliation” of evidence by failing to preserve critical communications with the insurer.

If you delete voicemails from the adjuster, lose the original denial letter, or wait until the statute of limitations runs out, the court will likely dismiss your case regardless of how egregious the insurance company’s conduct was.

Acting immediately allows us to send preservation letters that legally compel the insurer to preserve all data, preventing them from “losing” evidence of their own bad faith.

Demand the Best San Antonio Bad Faith Insurance Lawyer: Call 210-TREVINO Now

Carriers like State Farm, USAA, Farmers Insurance, Allstate, Geico, Progressive, and Fred Loya use algorithms to deny valid claims in the Loop 410 and Greater San Antonio area. They expect high-volume settlement mills to fold rather than go to trial. At Trevino Injury Law, we do not settle; we force them to pay. We fight for families, preparing every claim for a Bexar County jury.

Don’t Guess About Your Rights. Get a Definite Answer.

The insurance company is already evaluating your accident. Call 210-TREVINO Now to level the playing field, or choose your next step below. It’s confidential and you pay nothing unless we win.

Our trial-first aggression turned a $5,000 offer into a $536,000 verdict. Don’t let delays lead to the spoliation of evidence. As your dedicated San Antonio bad faith insurance lawyer, we immediately send preservation letters to secure critical adjuster logs. We fight on a strict contingency basis: No Win, No Fee.

Call 210-TREVINO for a free case review. Se Habla Español.